After 56 years of federal gridlock, the “Schedule I” era is officially over. On Thursday, April 23, 2026, Acting Attorney General Todd Blanche signed the historic order to reclassify marijuana as a Schedule III substance—a shift that fundamentally alters the financial DNA of every cannabis company operating on US soil.

For traders, this isn’t just a win for medical access; it is a direct strike against Section 280E, the tax code that has incinerated the cash flow of American multi-state operators for a generation. As the MSOS ETF bounces off a definitive technical floor on record-breaking volume, the market is no longer trading on “hope”—it is trading on the reality of net profitability. With an expedited hearing already scheduled for June 29, the window for analysing this structural pivot is narrow. Here is the factual breakdown of the news, the technical setup, and the cross-border battle for the multibillion-pound US market.

This is not investment or trading advice. If you lose your money, sue yourself!

1. The 2026 Policy Pivot: From Schedule I to Schedule III

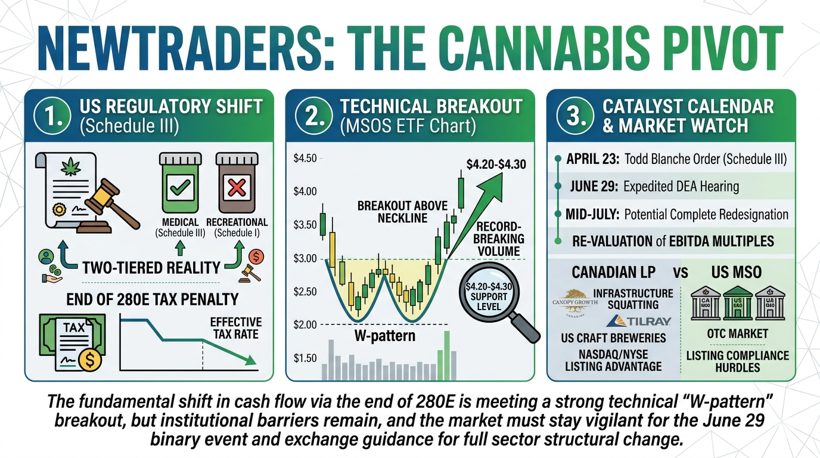

- 1.1 Understanding the Todd Blanche Order: On April 23, 2026, Acting Attorney General Todd Blanche signed an official DOJ order immediately moving state-licensed medical marijuana and FDA-approved cannabis products from Schedule I to Schedule III of the Controlled Substances Act (CSA). This reclassification places cannabis in the same category as ketamine and anabolic steroids, acknowledging its “currently accepted medical use” at the federal level for the first time in over five decades.

- 1.2 The Two-Tiered Reality: It is critical for traders to note that this order is surgically precise. While it legitimises state-regulated medical programs, it does not federally legalise recreational (adult-use) marijuana. Non-medical marijuana remains, for the moment, a Schedule I substance. This has created an unprecedented regulatory environment where the same product’s federal status depends entirely on the licence under which it was sold.

2. Fundamental Shifts: Beyond the Hype

- 2.1 The End of Section 280E: The primary driver of the recent stock surge is the removal of the IRS Section 280E tax penalty for medical operators. Previously, Schedule I status prevented businesses from deducting ordinary operating expenses (rent, payroll, marketing) from their federal taxes, often resulting in effective tax rates of 70% or higher. Under Schedule III, medical dispensaries are now permitted to make standard business deductions, a move expected to save the industry billions in annual cash flow.

- 2.2 Institutional Barriers: While the reclassification provides immediate tax relief, significant institutional barriers remain. Major US exchanges (NYSE/Nasdaq) still prohibit the listing of companies that “touch the plant” due to the remaining federal prohibition on recreational use. Furthermore, without the passage of the SAFER Banking Act, most tier-one banks still lack the legal “safe harbour” required to provide traditional commercial lending or custody services to the sector.

3. Analysing the Technical Floor

- 3.1 The MSOS “W-Pattern”: Looking at the AdvisorShares Pure US Cannabis ETF (MSOS), a clear double-bottom (W-pattern) formed between late 2025 and early 2026. This technical formation suggests a definitive floor has been established near the $2.00–$2.50 range after a multi-year bear market. The recent vertical breakout from this base indicates a transition from a phase of accumulation to an active uptrend.

- 3.2 Retests and Volume: The price action following the Todd Blanche order saw record-breaking volume—nearly eight times the daily average—confirming institutional conviction behind the move. While the market is currently consolidating around the $4.20–$4.30 support level, this “retest of the neckline” is standard technical behaviour. Maintaining this floor is crucial for validating the “big move up” ahead of summer catalysts.

4. The Cross-Border Setup: Canadian LPs vs. American MSOs

- 4.1 Infrastructure “Squatting”: Canadian Licensed Producers (LPs) have spent years positioning themselves for this moment. Canopy Growth (CGC) has established Canopy USA, a separate entity designed to “activate” US-based acquisitions like Wana and Acreage Holdings the moment federal rules permit. Similarly, Tilray (TLRY) has acquired US craft breweries to leverage existing American distribution networks for future THC-infused product lines.

- 4.2 The Exchange Hurdle: Despite the reclassification, a major hurdle remains: listing compliance. Because recreational marijuana is still Schedule I, American Multi-State Operators (MSOs) remain relegated to the OTC markets. Canadian firms currently hold a distinct advantage as they can maintain their Nasdaq and NYSE listings while “squatting” on US soil through non-plant-touching subsidiaries or options-based acquisition structures.

5. The Catalyst Calendar

- 5.1 The June 29 Hearing: The roadmap for the Department of Justice’s expedited administrative hearing begins on June 29, 2026. This hearing, overseen by the DEA, is specifically designed to evaluate the “complete redesignation” of marijuana. For traders, this is the binary event: a successful conclusion (expected by mid-July) could expand Schedule III status to the entire adult-use market, finally reconciling the state/federal conflict for the largest US operators.

- 5.2 Market Mechanics: Traders must distinguish between a sentiment-driven “dead-cat bounce” and a structural shift. Historically, cannabis rallies have faded due to a lack of fundamental change; however, the Schedule III reclassification provides a tangible, legislative catalyst that directly impacts earnings per share (EPS). As of late April, the consolidation above the previous multi-year resistance suggests the market is pricing in a long-term revaluation of the sector’s EBITDA multiples.

Conclusion

The shift from Schedule I to Schedule III represents a rare moment where a regulatory stroke of a pen fundamentally rewrites the valuation models for an entire sector. By effectively removing the 280E tax burden for medical operators, the federal government has replaced speculative “hope” with the cold reality of net profit and improved EBITDA multiples.

However, traders should remain vigilant; while the technical “W-pattern” on the MSOS chart suggests a long-term bottom is in place, the path to full federal legitimacy remains complex. The market is currently navigating a “two-tiered” legal landscape where the recreational market sits in a temporary regulatory shadow. Until the June 29 hearing provides a definitive roadmap for adult-use rescheduling and the major exchanges provide clear guidance on up-listing, volatility should be expected. The floor has shifted, but the final structural breakthrough is a binary event tied to the summer calendar.